The 2017 “Stall Point” and the Invisible ARPU Collapse

Telecommunications is the invisible foundation of the modern world. It is the central nervous system of global commerce, the substrate upon which the entire AI revolution is being built. Yet, beneath the surface of high-definition video streams and near-instantaneous global connectivity, the companies providing this foundation are in a structural tailspin.

For the last decade, the industry has been haunted by a brutal, mathematical reality: global population-weighted mobile Average Revenue Per User (ARPU) has declined by a staggering 45%. Consumers and enterprises are consuming more data than ever before, but they are paying less for it with every passing year. This persistent downward pressure has forced operators into a state of structural commoditization, where traditional network quality no longer provides a sustainable competitive advantage, and luring people into stores to buy additional gadgets is not a serious play.

Historical data indicates that the industry hit what analysts call the “2016-2017 Stall Point.” This was a structural inflection point where global revenue peaked at approximately $1.67 trillion and then entered a period of stagnation and declining growth rates. In 2016, 4G penetration was at its zenith in developed markets. By 2017, the decoupling of network usage from network revenue became absolute. While data volumes exploded, flat-rate data plans and the rise of Over-The-Top (OTT) applications—which replaced high-margin SMS and voice services with free alternatives—triggered a pricing “race to the bottom.”

This is the “Dumb Pipe” trap. Operators spend billions on capital expenditures (CapEx)—over $1.1 trillion globally on 5G infrastructure alone—only to find that technological upgrades historically fail to generate top-line growth. Instead, they merely maintain the status quo while users capture the value. We are witnessing the rise of a Commoditization Index (CI), where the market-share spread and ARPU spread have fallen below 25%, pushing 78% of studied countries into “Commoditized” zones.

As one enterprise Head of Growth Strategy recently noted in a strategic audit:

“I genuinely cannot tell you if that 45% premium is buying us actual intelligence differentiation or if it’s just the same cables with a shinier SLA document attached... we are locked into terms that benefit the operator. We pay more money just to watch the operator.”

The industry is now attempting a trillion-dollar pivot to escape this trap. It is a pivot that moves in two directions: upward into the stars through Non-Terrestrial Networks (NTN) and inward into the core logic of the network through Agentic AI.

Takeaway #1: The 45% “Intelligence Tax” You Didn’t Know You Were Paying

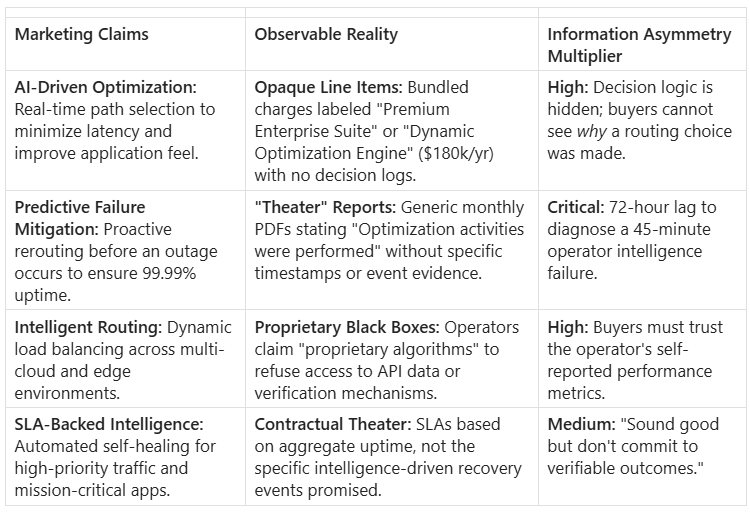

The most startling revelation from recent industry research is the scale of “Information Asymmetry” between telecom providers and enterprise buyers. Enterprises currently pay a massive premium—often 40% to 50% above baseline transport costs—for what is marketed as “intelligence.”

However, this intelligence is largely a “black box.” Operators use “proprietary IP” as a shield to deflect transparency, preventing buyers from verifying whether they are receiving optimized routing or just standard, commoditized connectivity. Transcripts from senior growth leaders reveal a “trust-based procurement” model that is essentially a billion-dollar structural failure.

As Marcus, a Head of Growth Strategy, noted:

“Every single operator comes in with these gorgeous slide decks about their AI-driven this... And I’m like, okay, show me the decision log... And they go quiet. It’s a tactic—they know we can’t prove it, so they hold firm on pricing.”

This “Intelligence Tax” is an unverified expense that persists because the operator controls the testing environment. To resolve this, enterprises must move toward Information Asymmetry Resolution (Lever #1): mandating operator disclosure of transport cost versus intelligence premium allocation.

Takeaway #2: Beyond Chatbots—The Rise of “TelcOS” (Agentic AI)

To escape commoditization, the industry is shifting from superficial AI experiments—like basic customer service chatbots—to a deep, “Agentic Execution Layer.” This paradigm, known as TelcOS, envisions the network not as a collection of hardware, but as an autonomous operating system.

Unlike traditional “Copilots” that suggest actions for human approval, Agentic AI consists of autonomous “Agents” capable of making real-time decisions with minimal human intervention. This shift is critical for protecting EBITDA margins as network complexity outpaces human management capabilities.

The Economic Engine of TelcOS:

Aggressive Market Forecast: Aggressive models suggest an Agentic AI in Telecom CAGR of 48.5% through 2034, potentially reaching a market size of $187.7 billion.

Cost Reduction: Shifting to AI-native operations can reduce IT costs by up to 30% by eliminating manual network orchestration.

Revenue Optimization: Integrated Customer Network Experience (CNX) indices allow operators to boost ARPU by 10% to 15% by linking network performance directly to user behavior and churn risk.

In a TelcOS environment, “Self-Healing Networks” use agents to analyze real-time telemetry across RAN (Radio Access Network), core, and transport domains. These agents adjust antenna patterns and load-balance protocols autonomously. The eventual “Hunch” shared by industry insiders is that by 2035, zero-touch network management will eliminate the need for human network planners and field dispatch teams entirely.

Takeaway #3: The Sky is No Longer the Limit (The D2D Revolution)

While AI transforms the network’s brain, Low Earth Orbit (LEO) satellites are transforming its reach. The Non-Terrestrial Network (NTN) horizon represents a fundamental shift in how we conceive of “coverage.”

The industry is moving away from specialized, expensive satellite phones toward Direct-to-Device (D2D) connectivity. Using 3GPP standards (Release 17 and 18), standard, unmodified smartphones can now connect directly to satellite constellations. This isn’t just a niche project; it is a mainstream strategy signed by over 91 operators globally.

The Growth Contrast:

Core Terrestrial Services: Sub-inflationary growth at a 2.8% to 2.9% CAGR (2024–2029).

Direct Satellite-to-Phone Services: Explosive 28.5% CAGR through 2034.

The T-Mobile and SpaceX partnership is the vanguard, covering over 1.9 million square miles that were previously dead zones. This enables the Industrial B2B IoT Edge—tracking assets in maritime, logistics, and agriculture across the 70% of the Earth’s surface that lacks cellular coverage. The “SpaceX Factor” assumes that satellite constellations will eventually commoditize terrestrial operators entirely, turning legacy telcos into basic billing and marketing agents.

Takeaway #4: The “Labor Inversion” – Paying to Watch Your Provider

One of the most provocative findings in recent strategic audits is the “Labor Inversion.” In this scenario, the enterprise buyer absorbs the operational costs that should be bundled into the provider’s service. Because operators are opaque about their “intelligence,” enterprises are forced to spend significant capital to monitor the very providers they are already paying premium rates.

The Inefficiency Math

To quantify this, we look at the Quantified Inefficiency Index. A standard enterprise engagement involves manual data reconciliation that bypasses the “Proprietary Shield.”

Labor Breakdown:

Data Intake: $114/hr (2 hours)

Analysis/Processing: $285/hr (4 hours)

Review/QA: $855/hr (1 hour)

Executive Sign-off: $1,710/hr (0.5 hours)

Total Cost per Reconciliation Run: $3,303

In a standard operating market with 5,000 runs per year, the Annual Waste per Unit reaches 16.5 million. For a single-client scale enterprise operating across 250 markets, this compounds into **4.1 billion in annual waste**.

“We have spent probably $200,000 on third-party monitoring tools... and our network team spends 60% of their time just trying to verify what operators are actually delivering. We are paying twice: once for the service, and once for the tools to watch the service.”

Furthermore, the “Abandonment Tax”—where 15% of measurement cycles are abandoned because they are too labor-intensive—results in $15.4 billion in stranded opportunity. Decisions are made on “faith” rather than evidence, leading to massive value leakage.

Takeaway #5: ASVR – The “North Star” Metric for the AI Era

In a world increasingly dominated by machine-to-machine traffic, the legacy metric of ARPU (Average Revenue Per User) is a “Legacy Blindspot.” Billing systems designed for human identities cannot capture the value generated by autonomous agents.

Enter the Autonomous Session Value Ratio (ASVR).

The Formula:

Strategic Rationale: Currently, machine traffic is systematically underpriced. If an operator generates 1 billion agent sessions monthly at 0.001/session, but those sessions deliver **0.05 in automation gains (efficiency, latency reduction, task completion), the operator is experiencing $49 million in monthly revenue leakage**.

The ASVR isn’t just a metric; it’s a Value-Pricing Hook. Closing the gap to an ASVR of 0.5 allows operators to unlock millions in revenue from existing infrastructure without adding a single new human subscriber. For the enterprise, ASVR provides the first rigorous framework to value-price the intelligence they are consuming rather than just “paying for the pipe.”

Takeaway #6: The $28.5 Trillion Prospectus (The SpaceX Factor)

The strategic pivot isn’t just about better cell service; it’s about a massive reconfiguration of global infrastructure. The SpaceX prospectus frames a Total Addressable Market (TAM) of $28.5 trillion by 2026, spanning AI, global connectivity, and space-enabled infrastructure.

One of the most intriguing strategic plays involves the repurposing of physical assets. Legacy telecom central offices—the old copper switching hubs found in every city center—are being eyed as the secret weapon for Edge AI compute nodes. These locations offer what hyperscalers lack: localized, low-latency power and space.

However, a cynical “industry hunch” persists regarding “Sovereign AI.” While marketed as a move toward nationalized data security and infrastructure independence, many analysts believe the narrative is primarily a regulatory play designed to extract state subsidies. Telcos are using national security concerns to secure public capital for data centers they cannot afford to build on their own. With 55% of Telecom CEOs believing their companies won’t be viable in 10 years, the rush to extract these subsidies is a survival mechanism.

The 13-Step “Friction Map” for Modern Procurement

For Enterprise Growth Strategy leaders, navigating this transition requires a rigorous approach to procurement. The following map highlights the critical steps to piercing the “Proprietary Shield” and reclaiming value.

FPI: Friction Priority Index. The architectural problem is quantified mathematically (Inefficiency Index) and then distributed across the job map logically (and scored — FPI). No consumer survey will ever be able to do this — they aren’t engineers and do not know your architectural constraints. And this is faster and far less expensive.

Assess Spend vs. Intelligence Value (FPI: 100): Minimize the likelihood of paying premium rates for undifferentiated transport. Use the 45% benchmark as a baseline.

Map Critical Operations (FPI: 64): Identify revenue-critical applications. Reduce attribution lag from 72 hours to near-real-time.

Research Observability Features (FPI: 64): Screen for operators who allow decision-logic transparency. Demand more than “glossy slides.”

Map Internal Stakeholders (FPI: 27): Align the 12-15 stakeholders (IT, Finance, Legal) on a shared vocabulary for “Intelligence.”

Mandate Intelligence Observability (FPI: 100 - CRITICAL): Prepare RFPs that require operators to expose their decision-logic APIs as a condition of contract award.

Audit Supplier Contracts (FPI: 100 - CRITICAL): Remove “contractual theater.” Replace vague “best effort” language with verifiable outcome requirements.

Validate Claims via Demos (FPI: 1): Demand outcome-verifiable routing demonstrations, not canned videos.

Negotiate Observable Pricing Tiers (FPI: 100 - CRITICAL): Use the ASVR to anchor pricing to automation gains. Don’t sign until the logic is visible.

Establish Buyer-side Observation (FPI: 100 - CRITICAL): Build internal instrumentation that correlates network intelligence events with business metrics. Stop the labor inversion.

Monitor Delivery (FPI: 64): Use automated dashboards to track decision path provenance, not monthly PDFs.

Escalate Failures (FPI: 64): Require operators to provide decision-logic evidence within defined timeframes for every outage.

Adjust Commercial Terms (FPI: 64): Ensure mid-term commercial elasticity. If the intelligence isn’t observed, the premium isn’t paid.

Document Outcomes (FPI: 64): Build a validated evidence package for renewals. Eliminate the 200-300 hours of manual “incomplete” data gathering.

Conclusion: The Final Thought-Provoking Question

The global telecommunications industry is undergoing a structural reconfiguration that will define the next twenty years of digital trade. The “2017 Stall Point” was the warning shot; the rise of TelcOS and NTN is the response.

However, the burden of proof has shifted. We have moved from a world where we pay for connectivity to a world where we pay for the intelligence that manages that connectivity. If you cannot observe that intelligence, you are not a strategic partner; you are a victim of information asymmetry.

As the industry pivots toward a $28.5 trillion future, the question for every C-suite leader isn’t whether the network is up—it’s whether you can see why it’s up.

Is your network intelligence an asset you can verify, or a magic trick you’re just paying to see?

Is your organization interested in true innovation? Or does it prefer to just look busy and hire consultants? The world is changing quickly. If you’re not adapting to it, you’re not innovating. I work with organizations who are serious about the subject and are willing to challenge the current paradigm. Is that you? (my availability is limited)

Book an appointment: https://pjtbd.com/book-mike

Email me: mike@pjtbd.com

Call me: +1 678-824-2789

Join the community: https://pjtbd.com/join

Follow me on 𝕏: https://x.com/mikeboysen

Articles - jtbd.one - De-Risk Your Next Big Idea

Always attack…Never defend