Over 20 years ago I spent 3 years in the insurance industry (a general agency). This is only important because the topic of this research is also related to the insurance industry. And more importantly, at that time I proved the exact thing that this research uncovers. Trust through visibility is the answer. I implemented a system that solved a huge problem for my employer.

We had an incessant flow of inbound inquiries from agents trying to get an update on the status of a client application. The research necessary to resolve kept our processing team from doing their job—processing new applications. The system I developed proactively sent these agents an update of the application status, which specialist now processing it, and the direct phone line and email address to that person.

I reported directly to the COO. He was skeptical, but allowed this to proceed. He had been routing all calls through a single dispatcher to manage the flow— it hadn’t been working. The volume was insane. I flipped the switch. Emails, faxes (no texting yet) at every change in status and hand-off. Fear gripped the executive suite. What happened?

The first week, in bound calls were down 85%. The process still took the same amount of time. The podcast goes into this—in-depth because it found the same problem I did. And no, I didn’t guide it that way.

Free Access to Research Artifact

If you point an LLM at the public internet, you get pattern-matching and slide-deck filler—a race to the middle executed at lightspeed. In modern strategy, the model is not the moat; the proprietary data payload you query is. To prove this, I’m opening my research vault: every week, I compile a complete, industry-wide research payload (job maps, physics floors, and inversion plans) into a secure Google NotebookLM workspace. If you have a Gmail account, you can enter the workspace, query the raw math, and stress-test the data yourself. Today’s artifact is about The Fallacy of Insurance CX

The global insurance industry is undergoing a structural paradigm shift, navigating an era of unprecedented consumer fluidity and transitioning away from an insulated ecosystem dominated by actuarial pricing. We are living in what analysts call the “Endurance Economy”—an environment defined by rising premiums due to secondary perils, sustained financial constraints, and an incredibly low tolerance for administrative friction.

In this hyper-competitive landscape, legacy carriers are desperate to win on Customer Experience (CX). But there’s a massive, expensive problem: the vast majority of them are solving the wrong equation.

Insurance executives love to believe that a fast payout equals a happy customer. It sounds logical, it looks great on a steering committee slide deck, and it justifies massive IT budgets dedicated to shaving days off the adjudication cycle. However, a deep dive into the structural economics of the Insurance CX industry reveals a completely different reality. The core battleground has migrated. Consumers today benchmark their insurance carriers not against other legacy providers, but against frictionless digital-native tech giants and consumer retail brands.

In this environment, the claims experience has evolved into the industry’s primary “trust engine”. Yet, carriers are burning $60 million in direct operational expense and stranding a staggering $495 million in policyholder relationship value annually because their post-loss claim status visibility is structurally broken.

Here are the most surprising, counter-intuitive, and impactful takeaways from the front lines of the insurance CX revolution—and why everything you thought you knew about claims satisfaction needs a radical reset.

The “Visibility Lie” (Why Speed Doesn’t Equal Trust)

The most dangerous belief inside the insurance C-suite today is that settlement amount and raw payout speed are the only things customers care about. This belief is expensively wrong.

Policyholders actually evaluate carriers on the perceived transparency, speed, and emotional friction of the restitution journey. The dollar amount of the settlement is merely the price of admission; the continuous visibility into how that settlement is being computed is the actual product.

To understand this, you have to look at the math governing a claims operation. A claim isn’t just an emotional event; it is an inventory dynamic governed by Little’s Law ( L = λ * T ), where the in-flight claim inventory scales linearly with the claim arrival rate and resolution time. When catastrophic events occur, arrival rates spike, sub-queues saturate, and resolution times balloon.

During these waits, the absence of visibility damages the relationship irreparably. The industry suffers from a 33% process abandonment rate, meaning one in three in-flight claims abandons the queue entirely due to opacity, resulting in policyholders disengaging mid-process and walking away at renewal. A policyholder who knows exactly where their claim sits in the queue will tolerate resolution times 40–60% longer than a policyholder kept in the dark.

“Loudest isn’t worst. Worst is quiet... our internal systems are most fragmented in the middle of the process.”

Carriers have incredibly rich data—dozens of internal actuarial codes and system checkpoints—but project only a fraction of that reality to the policyholder. This “visibility lie” guarantees that customers are left panicking in a black box, proving that post-loss financial restitution requires continuous status visibility over mere operational speed.

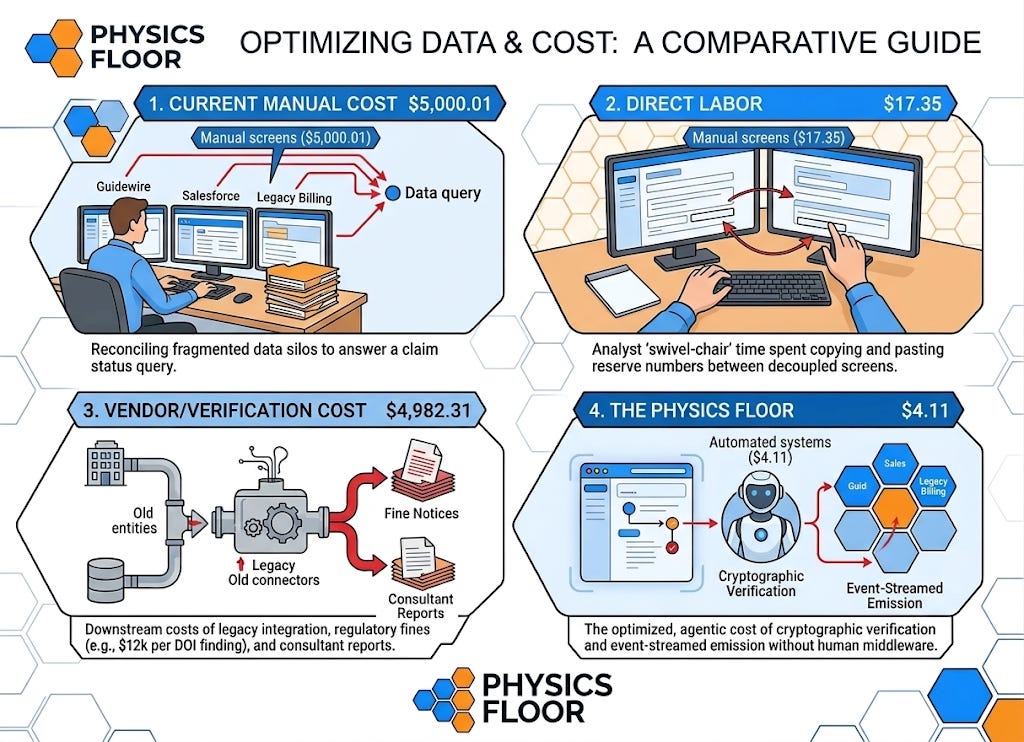

The 1,217x Inefficiency Multiplier (The $5,000.01 Execution Cost)

If you want to know why insurance premiums are rising, look at the cost of answering a single question: “Where is my claim?”

Currently, the cost to execute a single claim status governance action—producing, reconciling, and communicating a credible status update across federated legacy systems—runs a staggering $5,000.01.

What makes this number shocking is the breakdown. Only $17.35 of that cost is direct labor (an analyst physically pulling data). The remaining $4,982.31 is external resource and vendor verification cost. This includes massive Total Cost of Ownership (TCO) outlays for enterprise API gateways like MuleSoft, compliance audit fees, and the sheer operational friction of trying to bridge decades-old COBOL mainframes with modern CRM layers like Salesforce.

Because humans act as the “swivel-chair” middleware between siloed systems, the industry operates at an Inefficiency Multiplier of 1,217x above the physics floor. This structural waste bleeds $59.95 million annually for a baseline regional enterprise handling just 12,000 runs.

The “Tagging Tax” and the Rapid Decay of Information

To deliver visibility, you first have to know where your data lives. But in modern insurance, the data source inventory process is arguably the most punishing bottleneck in the entire ecosystem.

When a carrier attempts to catalog every system touching a claim—policy admin, billing, actuarial risk engines, and CRM platforms—it requires a massive manual effort. Because no single system holds the canonical truth, senior analysts must spend 400 to 500 person-hours of “stolen time” per cycle just to draft a list of data sources.

Worse yet, the industry attempts to solve this with capital expenditure. Carriers frequently spend $140,000 to $180,000 on static consultant reports to assess their claims data landscape. But these expensive artifacts rot within 90 days. Because CRM schema changes and legacy system updates occur silently, the inventory is perpetually out of date.

“We did a small engagement with... a data catalog vendor. Spent — I want to say — about $85K, and we got a really beautiful dashboard that nobody uses because it requires manual tagging.”

This “Tagging Tax” kills downstream initiatives. The exhaustive enumeration of data is a methodology violation; instead of mapping every schema, carriers should focus only on the 8 to 12 canonical claim states that actually drive 90% of policyholder status queries.

The 1.02 Elasticity Trap (Why AI Copilots Will Break Your Back Office)

It is highly intuitive to think that deploying Artificial Intelligence (AI) copilots and Robotic Process Automation (RPA) will fix the visibility crisis. This is “Pathway B”—the Sustaining Innovation play. But there is a hidden mathematical trap waiting for every carrier that tries this.

In claims status governance, the Jevons Elasticity Factor (E ) is exactly 1.02. This means the demand for visibility is slightly elastic relative to cost.

When you make it cheaper and easier for a policyholder to check their claim status (by introducing an AI chatbot, for example), they don’t just consume the same amount of information for less money. They ask more questions, more frequently. Because E ≥ 1.0, this creates a brutal “rebound trap”.

The volume growth completely consumes the efficiency savings, and the bottleneck simply shifts down the pipeline to the next human in the loop—usually the highly-paid senior claims reviewers adjudicating exceptions. Your operational expense collapses on the front-end communication line, only to explode at the adjudication-review line.

While AI copilots are a necessary “funding bridge” to buy runway and habituate users to algorithmic assistance, they cannot structurally close the 1,217x inefficiency gap because humans remaining in the execution loop impose a permanent cost floor.

The “Silent Divergence” (Loudest Doesn’t Mean Worst)

If you track customer complaints, you will inevitably see that the loudest, most aggressive feedback centers around final settlement amounts and payment timing. But optimizing exclusively for these loud complaints is a strategic error.

The most dangerous divergence between carrier reality and policyholder belief happens in the “Quiet Middle”.

During phases like inspection scheduling, peer review, and subrogation, the claim falls into an administrative black hole. The policyholder has no idea what is happening, but because they don’t know what they are supposed to be waiting for, they don’t complain.

Instead, they silently lose trust. This silent divergence is where the belief damage compounds, eventually resulting in the 33% process abandonment rate. By the time the customer calls to scream about the payout amount, the relationship was already destroyed three weeks prior in the quiet middle.

Please note: The system (and platform) require that several validation gates be used in order to justify the next stage. I bypassed those for this example. My client work requires a more rigorous and tightly scoped problem statement and goes beyond basic OSINT research.

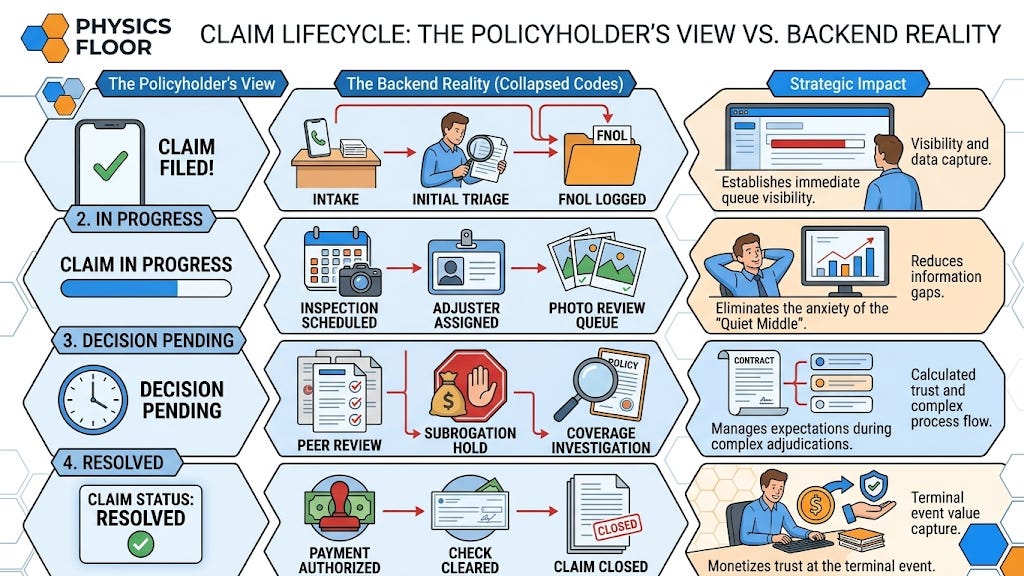

Escaping Consensus Theater: From 40 Codes to 4 States

Perhaps the most absurd reality of the insurance industry is the political gridlock over vocabulary. What does the term “in-flight claim” actually mean?

To an actuary, it means a transaction with an open reserve. To an operations manager, it’s a workflow state. To a CRM analyst, it’s a customer interaction. Getting these disparate stakeholders to agree on a universal definition results in “Consensus Theater”—a 4-to-9 month alignment cycle consisting of endless steering committee meetings and external facilitator costs reaching $40,000 per cycle.

“Getting alignment on the definition took — and this is embarrassing — eight months. Eight months, monthly steering committee meetings, and we still don’t have a universal definition.”

The solution to this political deadlock is a radical “Agentic Inversion”. Carriers must stop trying to achieve universal consensus on 40+ granular internal actuarial codes. Instead, they must deploy a read-only projection layer that completely bypasses legacy IT constraints.

By scraping event-state signals from system logs, this layer translates dozens of confusing, jargon-heavy internal codes into exactly four binary, outcome-oriented states that policyholders actually care about.

By vesting authority in a single Claims Restitution Experience Owner with an “opt-out veto” model, carriers can bypass the 7-department approval process and ship status updates in 48 hours instead of 9 months.

The Future of Claims is Transparent Governance

The $604.45 million strategic unlock waiting inside enterprise carriers won’t be captured by paying claims faster or by wrapping a 40-year-old COBOL mainframe in a shiny new chatbot interface. It will be captured by the carriers who realize that visibility is not a customer service initiative, but a queue governance mandate.

By decoupling the visibility layer from legacy cores, moving to a read-only event stream, and collapsing massive internal complexity into four simple states, forward-thinking insurers can invert the economics of the industry.

If your policyholders are waiting in a black box, what else are they silently abandoning while you optimize your payout speed?

Is your organization interested in true innovation? Or does it prefer to just look busy and hire consultants? The world is changing quickly. If you’re not adapting to it, you’re not innovating. I work with organizations who are serious about attacking problems and who are tired of defending the current paradigm. Is that you? (my availability is limited).

Submit a problem or challenge: Click here

Book an appointment: Click here

Email me: mike@pjtbd.com

Call me: +1 678-824-2789

Join the community: Click here

Follow me on 𝕏: https://x.com/mikeboysen

Articles - jtbd.one - De-Risk Your Next Big Idea

Always attack…Never defend