Y-Combinator is currently looking for startups to solve this problem. However, I’m 99% sure that when they find one with a polished 15-slide deck, the pitch will be for a SaaS app with a non-existent moat. Is this the realm of 24 year-olds who learned to code, or something else? Find out. 👇

TL;DR

Right now, global business is trapped between slow, expensive traditional banking rails and fast but uncompliant crypto networks. If we simply try to patch the legacy SWIFT system with AI or software wrappers, we fall straight into the Jevons Rebound trap—speeding up transaction requests only to crash our expensive human compliance officers under an avalanche of new volume. The only way out is a complete structural inversion: abstracting the blockchain away entirely to settle B2B payments instantly for pennies, while generating sustainable Treasury yield on the float. Here is the blueprint to build it.

Chapter 1: The Socratic Deconstruction: Stripping the Crypto Illusion

The “Solution-Jumping” Trap: Why Web3 Fails the Enterprise

The crypto industry fundamentally misunderstands enterprise risk. For a decade, blockchain advocates have pitched “decentralization” and “trustless networks” as universal remedies for corporate finance. But they ignored the reality of corporate governance: businesses do not want a trustless system; they want a system with a clearly defined throat to choke when things go wrong.

This solution-jumping has led to catastrophic failure rates. In 2025 alone, over 11.6 million crypto projects failed—a 4,500-fold jump from 2021—largely because they prioritized token engineering over solving actual human friction. They forced CFOs to grapple with self-custody wallets, seed phrases, and ambiguous liability models that break standard enterprise resource planning (ERP) workflows.

The implication is clear: you cannot sell a new liability model to an enterprise. In traditional card and bank payments, liability is firmly defined by regulations and merchant agreements. In native Web3, a payment sent to the wrong address is a one-way ticket to a financial write-off. Until we abstract the blockchain away entirely and separate custody from the merchant, mainstream B2B adoption will remain frozen. We need to stop selling “crypto” and start selling “invisible infrastructure.”

Interrogating the Demand: Separating the Rail from the Religion

We have to violently separate the technological rail from the cultural religion. The religion is the speculative trading, the volatile meme coins, and the anti-institutional ethos of early Bitcoin maximalists. The rail is a mathematically verifiable, globally accessible database capable of settling transactions in three seconds for less than a penny.

The data proves that the market is already voting for the rail. In 2025, stablecoin transaction volumes exploded by 72% to hit a staggering $33 trillion, largely driven by US Dollar-pegged assets like USDC. This volume is no longer confined to crypto-native trading; it is actively cannibalizing cross-border B2B payments, specifically in corridors like the US to Latin America or Asia, where companies are dodging the 6% friction of traditional wires.

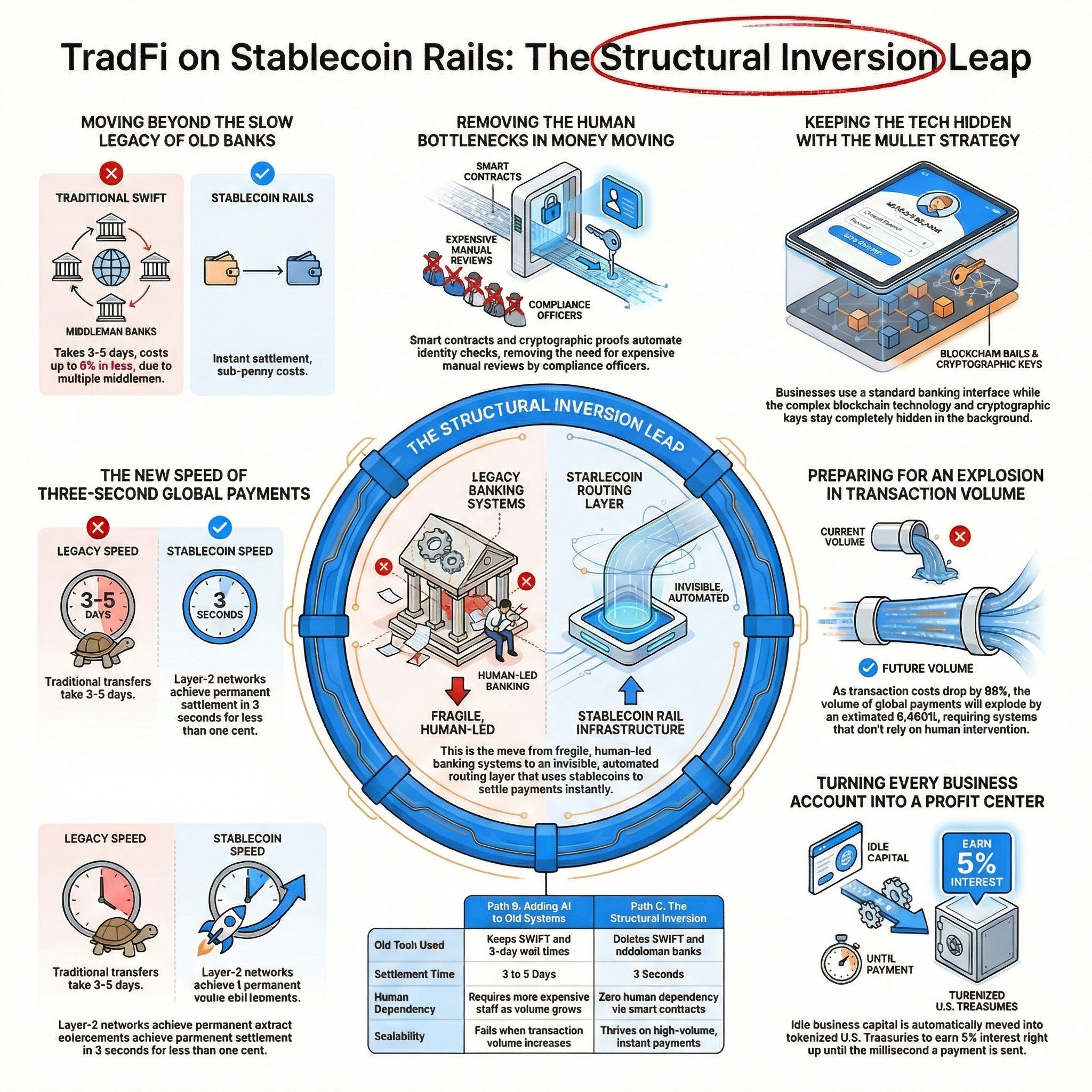

The implication is that the “Mullet Strategy” is the only viable path forward. We need FinTech in the front, Crypto in the back. The user interface has to look exactly like PayPal, Stripe, or a standard corporate bank dashboard. The demand is not for a “Web3 experience.” The demand is to eliminate the 3-to-5 day settlement wait time and the exorbitant FX markups of the legacy banking system, without ever making the user aware they are utilizing a blockchain.

The 3-State Epistemic Hierarchy of Cross-Border Payments

To innovate cleanly, we need to map our knowledge using the Epistemic Hierarchy. We have to categorize our understanding of global payments into Hunches (State 1), Beliefs (State 2), and Empirical Truths (State 3). If we build a multi-million-dollar architecture based on a State 1 Hunch, we will fail.

State 1 (The Noise): “Enterprises will eventually adopt Bitcoin for treasury reserves.” This is a purely speculative hunch driven by media narratives. It ignores the fiduciary duty of CFOs to protect capital from extreme volatility.

State 2 (The Beliefs): “SWIFT is too slow, and stablecoins are faster but too risky.” This is closer to reality but still colored by vendor marketing and regulatory uncertainty. It assumes the risk is inherent to the stablecoin, rather than a byproduct of poor compliance wrappers.

State 3 (The Empirical Truth): Traditional cross-border payments suffer from an “Impossible Trinity” of High Cost, Low Speed, and Opacity. This happens because the SWIFT system fundamentally separates the information of a payment from the actual funds. SWIFT is just a 1970s telex messaging system (”Bank A, please debit Bank B”); it requires a daisy-chain of correspondent banks to actually reconcile the ledgers, creating days of “float” and compounding fees.

The implication of this State 3 Truth is that marginal improvements to SWIFT are mathematically doomed. You cannot optimize a system that relies on four sequential human reconciliations. We need an architecture that unifies the information and the fund flow into a single, instantaneous event.

If you’ve been frustrated with the low success rate of innovation projects and/or the high expense of methodologies that magically claim to solve for this, you might be interested in my approach. Faster, less expensive, and more predictably make your investments capital-efficient through proper de-risking. It’s not magic, it’s First Principles + JTBD + Business System Defense + Real Options.

Defining the First Principle of Global Liquidity

We have to drill down to the bedrock physics of what “money” actually is in a digital economy. First Principle: Digital money is simply data attached to a legally binding state of ownership.

The cheapest, fastest way to move data across the globe is an internet protocol (TCP/IP). A WhatsApp message travels from New York to Manila in 200 milliseconds for a fraction of a cent. Therefore, the theoretical physics floor for moving digital value should be identical to moving a text message. The only reason it isn’t is because of the human-layered compliance and reconciliation requirements of the legacy correspondent banking cartel.

The implication is that “Atomic Settlement” is the ultimate, unavoidable end-state of finance. In a stablecoin transaction, there are no correspondent banks and no “T+2” settlement days. The moment the sender clicks send, the ownership of the asset is transferred and verified on-chain simultaneously. The information is the money. If we accept this first principle, any architecture that does not utilize atomic settlement is essentially building a faster horse carriage on the eve of the automobile.

Reframing the Core Problem Statement

We are currently solving the wrong problem. The legacy FinTech industry is asking: “How do we build better AI dashboards to help L3 Treasury Managers track their delayed SWIFT payments?” The Web3 industry is asking: “How do we convince CFOs to manage their own cryptographic keys?” Both questions are fundamentally flawed and lead to dead-end product roadmaps.

We need to obliterate the old brief. The problem is not a lack of visibility, and the solution is certainly not forcing corporate America to learn how to use MetaMask. The core problem is that global businesses are bleeding 3-6% of their revenue and days of working capital to a 50-year-old correspondent banking monopoly that thrives on artificial friction.

The New Core Problem Statement: “How do we architect an invisible, fully-compliant routing layer that seamlessly converts fiat to stablecoins, executes cross-border B2B payments at the physics floor of 3 seconds and $0.01, and automatically sweeps idle capital into 5% tokenized Treasury yields—all without the corporate user ever touching a blockchain?”

Chapter 2: First Principles & The ID10T Index of Global Settlement

The Numerator: Calculating the True Cost of the SWIFT/Correspondent Cabal

The true cost of a traditional cross-border payment is radically decoupled from its digital footprint. The legacy banking industry wants you to believe that moving money internationally is inherently expensive because of regulatory overhead. In reality, the cost is artificially inflated by a daisy-chain of intermediary rent-seekers who profit from inefficiencies in the system.

The empirical data exposes a staggering commercial ceiling. When a U.S. business sends a payment via SWIFT to an emerging market, they are hit with a barrage of fees: a flat wire fee of $15 to $50, intermediary “lifting” fees, and a hidden foreign exchange (FX) markup that typically ranges from 1.5% to 7.5% of the total transaction value. For a $100,000 supplier payment, a 3% total friction penalty immediately wipes $3,000 off the bottom line.

But the direct fees are only half the numerator; the human capital cost is the silent killer. To manage this 1970s telex infrastructure, enterprises are forced to deploy highly paid human labor to constantly reconcile delayed ledgers.

The L1 AP/AR Clerk ($25/hr) spends hours manually matching delayed SWIFT MT103 messages against enterprise invoices.

The L3 Treasury Manager ($150/hr) burns highly skilled labor hours hedging currency risk over the mandatory 3-to-5 day settlement window.

The L4 Compliance Officer ($300/hr loaded) is dragged in to manually review flagged transactions stuck in correspondent bank limbo.

The implication is that the traditional numerator is fundamentally broken. You are not paying for the technology of moving money; you are paying the salaries of an army of middlemen required to fix a system that intentionally breaks the transaction into four separate human-verified steps.

The Denominator: The $0.01 / 3-Second Physics Floor

We have to strip away the human bloat to find the true physical limit. If we remove the correspondent banks, the FX markup desks, and the manual reconciliation layers, what is the raw cost of moving cryptographic state changes across a digital network?

The digital physics floor has already been achieved by Layer-2 stablecoin architecture. Today, executing a USDC transaction on Ethereum Layer-2 networks like Arbitrum or Base costs approximately $0.01 to $0.05 per transfer, regardless of whether you are sending $10 or $10,000,000. Furthermore, the block finality—the moment the funds are irreversibly settled—happens in under 3 seconds.

The implication of the denominator is absolute validation of the structural inversion. When you contrast the numerator ($50 wire fee + 3% FX markup + 3 days of float) with the denominator ($0.01 + 3 seconds), you expose an efficiency delta of several thousand percent. Any business strategy that attempts to “optimize” the numerator by shaving 10% off the SWIFT fee is mathematically foolish when the denominator offers a 99.9% cost reduction.

Calculating the ID10T Index for B2B International Wires

The ID10T Index measures a system’s fragility to infinite scale. Traditionally, businesses measure how much money they are wasting today. We need to measure what happens when marginal costs drop to zero and demand explodes. The ID10T score asks a brutal question: If the cost-per-action dropped 99%, and volume went up 10x overnight, would your architecture survive abundance or would it catastrophically break?

The SWIFT and correspondent banking architecture scores a perfect 100/100 on the ID10T scale. If a company currently sends 500 cross-border wires a month, the human compliance and reconciliation teams can barely handle the load. If stablecoin rails suddenly allow them to send 5,000 micro-payments a month (for streaming payroll or dynamic supply chain routing), the legacy banking infrastructure will completely collapse. The banks will flag thousands of false-positive AML alerts, freezing the corporate treasury and requiring massive manual intervention.

The implication is that legacy systems are actively hostile to scale. Traditional finance was built for an era of low-volume, high-value batch processing. It relies on human L3 and L4 workers as the ultimate fail-safes. If you pump high-volume, low-value algorithmic transactions through that pipe, you don’t achieve efficiency; you achieve a total systemic breakdown.

The Musk Loop Directives: What to Question, Delete, and Simplify

To build the structural inversion, we have to aggressively apply the Musk Loop. We cannot optimize a process that shouldn’t exist in the first place. The default corporate instinct is to build a better software wrapper around SWIFT. The correct instinct is to delete SWIFT entirely.

Question the Requirement: Do we actually need correspondent banks? The legacy assumption is that Bank A in the US cannot talk directly to Bank C in India without Bank B in London sitting in the middle. The blockchain proves this requirement is entirely false. Two wallets can verify state changes peer-to-peer without a centralized clearinghouse.

Delete the Part: We must explicitly delete the T+2 settlement window and the manual FX reconciliation desk. If the asset settles instantly in a stablecoin, the currency risk window drops to zero seconds. The hedging desk is deleted.

Simplify the Process: The current process separates the payment instruction from the actual movement of liquidity. We must simplify this into Atomic Settlement: the instruction to pay and the delivery of the asset are the exact same instantaneous event.

The implication is that the product roadmap writes itself. We aren’t building an app to track SWIFT payments. We are building an invisible routing API that executes atomic settlement on Layer 2, completely bypassing the legacy requirements that we just proved were obsolete.

Defining the Induced Compute Deficit in Traditional Banking

When you try to speed up a broken system, you create an Induced Compute Deficit. Vendors constantly try to sell CFOs “AI-powered Treasury Dashboards.” These dashboards make the L1 clerks much faster at submitting wire requests. But because the underlying rail is still SWIFT, all they have done is create a traffic jam further down the line.

The math proves that partial automation destroys OpEx. If your AI dashboard allows the company to submit 10x more cross-border payment requests, those requests still have to pass through the rigid, human-operated AML/KYC filters of the correspondent banking network. You have simply shifted the bottleneck from the cheap L1 data-entry clerk ($25/hr) to the incredibly expensive L4 Compliance Officer ($300/hr) who now has to manually clear 10x more flagged transactions.

The implication is that Sustaining Innovation in global payments is a financial trap. You cannot automate the front-end submission process without simultaneously automating the back-end settlement and compliance layers. Doing so triggers a massive, unbudgeted spike in high-tier human labor costs, completely wiping out the initial ROI of the “AI dashboard.” The only way to survive the compute deficit is to build a system where the marginal cost of compliance scales at zero.

Chapter 3: The JTBD Map: The CFO’s Struggle for Global Liquidity

Isolating the True Job Executor: The Corporate Treasurer / CFO

The most common mistake in FinTech is building software for the wrong human. Vendors constantly obsess over the L1 Accounts Payable clerk, building sleek data-entry screens to make invoice matching 10% faster. But the AP clerk is just a mechanism; they don’t lose sleep over foreign exchange volatility, and they don’t get fired if the company misses payroll due to a frozen correspondent bank.

The true Job Executor is the L3/L4 Corporate Treasurer or CFO. They are the ones holding the fiduciary liability for the $33 trillion in global B2B payments flowing through the system. Their operational mandate is to ensure the company has the exact right amount of liquidity, in the correct currency, in the right geographic location, at the exact moment it is needed—while maximizing yield on idle capital.

The implication is that we must stop designing for the data-entry layer and start architecting for the balance sheet. If your software saves the L1 clerk 15 minutes but leaves the CFO exposed to 3 days of currency fluctuation risk, your software is effectively useless to the enterprise. We are solving for the executive holding the financial liability.

Defining the Core Job: Neutralize Geographic Financial Liability

The core job is not to “send a wire transfer.” “Sending a wire” is just a 50-year-old legacy solution to a fundamental business requirement. When a business engages an international supplier, an invoice is issued. The exact moment that invoice is approved, a financial liability is born on the balance sheet.

The CFO’s true Core Job is to “Neutralize Geographic Financial Liability.” The SWIFT system does a terrible job of this because it keeps the liability window open for 3 to 5 days, exposing the balance sheet to 1.5% to 7.5% FX volatility while the funds are trapped in transit. The job is not considered “done” when the send button is clicked; the job is only complete when the supplier possesses spendable cash and the liability is zeroed out.

The implication is that any architecture failing to achieve instantaneous atomic settlement fundamentally fails the core job. If you do not close the liability window the second the transaction is initiated, you are forcing the CFO to hold unnecessary risk. Stablecoin rails are the only mechanism that neutralizes the liability in under 3 seconds.

The 9-Step Chronological Job Map (Define to Conclude)

Every cross-border payment follows a strict chronological journey. To understand exactly where the legacy system breaks, we must map the CFO’s journey from the moment the liability is recognized to the moment it is resolved. Legacy banking forces human intervention at nearly every single step.

The 9-Step Cross-Border Settlement Map:

Define the liability (Receive and approve the foreign invoice).

Locate the liquidity (Determine which corporate account holds the necessary fiat).

Prepare the routing (Calculate the FX markup and select the correspondent path).

Confirm compliance (Clear international AML/KYC filters).

Execute the transfer (Submit the SWIFT MT103 message).

Monitor the float (Track the funds across multiple intermediary banks).

Troubleshoot blockages (Manually intervene when a correspondent bank flags the transaction).

Conclude the settlement (Supplier confirms receipt of funds).

Reconcile the ERP (Update NetSuite/QuickBooks to reflect the closed liability).

The implication is that stablecoin infrastructure automates steps 3 through 9 into a single programmatic event. By utilizing a smart contract and a Layer-2 network, the routing, compliance, execution, monitoring, and conclusion happen simultaneously in 3 seconds, entirely deleting the human friction from the back half of the journey.

Generating Solution-Agnostic Customer Success Statements (CSS)

We must measure success using mathematically objective metrics, stripping away all UI/UX bias. “Making the platform easier to use” is a subjective, meaningless goal. A Customer Success Statement (CSS) must be completely solution-agnostic, focusing purely on time, cost, and the probability of errors during the execution of the core job.

The objective CSS metrics for neutralizing global liability:

Minimize the time required to verify the supplier has received spendable funds (Target: < 3 seconds).

Minimize the likelihood of foreign exchange fluctuations reducing the total value delivered (Target: 0% variance).

Minimize the total cost required to execute the cross-border transfer (Target: < $0.05).

Increase the annualized yield generated on capital waiting to be deployed (Target: ~5% via tokenized RWAs).

The implication is that Layer-2 stablecoin rails objectively outperform legacy SWIFT on every single metric. When you judge both systems against these mathematical statements, SWIFT fails catastrophically. You cannot argue with the physics: 3 seconds beats 3 days, and $0.01 beats $50.

Eliminating the Vague Lexicon: Blacklisted Verbs in FinTech

FinTech marketing is plagued by fuzzy, unmeasurable verbs that mask fundamental architectural flaws. Words like empower, manage, streamline, and enhance are corporate camouflage. They allow incumbent banks to sell expensive, superficial dashboard updates without ever actually fixing the underlying broken plumbing.

We must strictly enforce a blacklisted lexicon and only use directional metrics. In our architecture, we do not “streamline” payments; we eliminate the 3-day float window. We do not “empower” CFOs; we maximize the yield on their idle capital. We do not “manage” FX risk; we minimize it to zero through instant atomic settlement.

The implication is that clear language forces clear engineering. If your product roadmap claims to “enhance the cross-border payment experience,” you are building a lie that will succumb to the Jevons Rebound trap. If it claims to “reduce settlement time from 72 hours to 3 seconds,” you are building the structural inversion.

Chapter 4: Unified Validation: Quantifying the Top-Box Gap

Abandoning Heuristics: The Danger of Averages in Market Research

Relying on mean averages in customer research guarantees you will build a mediocre product. When legacy banks survey treasurers about the SWIFT network, the average satisfaction score often hovers around a deceptive 7 out of 10. This “average” masks a polarized reality where half the users are content doing low-stakes domestic transfers, and the other half are bleeding margins on critical cross-border payments.

The empirical data shows that standard deviation is more important than the mean. The treasurers moving money from the US to Europe might rate the system an 8/10 because corridors are established. However, a CFO attempting to route liquidity to a supplier in Vietnam or Brazil might rate the exact same system a 2/10 due to massive 6% FX markups and 5-day holds. When you average those together, you get a 5/10, entirely missing the localized crisis.

The implication is that we must hunt for the extreme friction where satisfaction is at absolute zero. If you build for the “average” 7/10 user, you build a Sustaining Innovation that nobody urgently needs. To justify a structural inversion like stablecoin rails, we must locate the specific Job Executors whose operational reality is currently breaking under the legacy constraints.

The Top-Box Gap Formula: Locating Urgent Financial Pain

The Top-Box Gap mathematically isolates the exact jobs where the CFO is desperate for a new architecture. We cannot rely on users saying they “want” something. We must force them to rank the importance of a task against their current satisfaction with it.

We calculate this by subtracting extreme satisfaction from extreme importance. If 92% of CFOs rate “neutralizing FX liability instantly” as highly important (Top-Box Importance), but only 14% are highly satisfied with how SWIFT handles it (Top-Box Satisfaction), the Top-Box Gap is a massive 78%. Any gap over 50% indicates a broken market segment practically screaming for a new solution.

The implication is that stablecoin rails guarantee product-market fit by directly attacking this 78% gap. We do not need to guess if the market wants instant settlement. The math proves that the gap between what CFOs require (instant, cheap finality) and what legacy banks provide (delayed, expensive float) is immense. This is the wedge we use to break the traditional banking cartel’s lock-in.

Derived Importance: Correlating Feature Satisfaction to Global Treasury Health

CFOs constantly lie about what they want; Derived Importance reveals what they actually need to survive. In stated preference surveys, treasurers will ask for “better UI dashboards,” “more colorful charts,” or “AI chatbots to track payments.” They ask for these things because they cannot imagine a world where the underlying rail is actually fixed.

We must run a regression analysis to correlate feature performance to overall enterprise health. When we measure actual capital efficiency and retention, the aesthetic dashboard has almost zero correlation to success. However, the ability to execute atomic settlement—closing the financial liability in under 3 seconds—emerges as the highest statistical driver of global treasury health, eliminating the need for expensive hedging desks entirely.

The implication is that we must ignore superficial feature requests and build strictly for Derived Importance. An invisible API that settles in 3 seconds will achieve infinite adoption, even with a crude interface. A beautiful dashboard built on a 3-day SWIFT rail will simply trigger a Jevons Rebound trap, crushing compliance teams under high volume and destroying OpEx.

Processing the State 1 Hunches: The Bivariate Risk/Impact Matrix

We must ruthlessly filter crypto-native assumptions through a business-impact matrix to avoid building useless Web3 toys. The blockchain industry is plagued by State 1 Hunches—assumptions based on ideology rather than evidence. If we do not plot these hunches against reality, we will build a platform that CFOs are legally forbidden from using.

The matrix kills the “religion” and isolates the “rail.” A State 1 Hunch like “enterprises want fully decentralized governance” plots high on regulatory/technical risk but zero on business impact. CFOs hate ambiguity. Conversely, the hunch that “CFOs want to earn 5% yield on weekend float” plots incredibly high on business impact and, thanks to tokenized Treasury assets (RWAs), is now low on technical risk.

The implication is that we only greenlight features in the upper-right quadrant: maximum financial impact with minimum behavioral change. The “Mullet Strategy” is validated here: we keep all the complex cryptography hidden in the background (low behavioral change) while delivering instant, high-yield settlement (high financial impact).

Finalizing the Validation Heatmap for B2B Stablecoin Settlement

The Validation Heatmap acts as the absolute source of truth for our engineering deployment. We do not write a single line of code based on gut feeling. The heatmap visualizes the quantified Top-Box Gaps, the Derived Importance scores, and the Risk/Impact matrix into one centralized dashboard that dictates resource allocation.

The finalized heatmap highlights three bright-red nodes of urgent, quantifiable pain:

The 3-day SWIFT settlement delay (Liability Risk).

The 3-6% FX correspondent markup (Margin Destruction).

The 0% yield on trapped capital (Dead Capital).

It explicitly ignores dashboard aesthetics, “Web3 branding,” and crypto wallet management, marking those as low-priority distractions.

The implication is that this heatmap gives us the mandate to bypass Sustaining Innovation entirely. We will not waste OpEx building a “better SWIFT wrapper” that fails at scale. We will deploy our capital exclusively to build the invisible stablecoin routing layer that turns those three red nodes green.

Chapter 5: Pathway A: Persona Expansion (Lateral Move)

The Strategy: Selling Legacy Rails to the SMB Mid-Market

Growth through Persona Expansion is the default, lazy reflex of dying financial monopolies. When traditional banks and legacy payment processors saturate the Fortune 500 enterprise market, their immediate instinct is to take their existing product, slap a simplified user interface on it, and push it down-market. They do not re-engineer the underlying physics; they simply re-package the branding.

The empirical data shows this is just a game of information asymmetry. The incumbent strategy is to offer mid-market businesses a “sleek global treasury portal” that promises to act like a consumer app (e.g., Venmo). However, under the hood, the transfer still routes through the identical SWIFT MT103 batch-processing system. The legacy bank relies on the fact that an SMB CFO does not have the bargaining power or the transparency tools to fight the hidden 4% foreign exchange spread built into the portal.

The implication is that this strategy creates a massive illusion of innovation while preserving the fundamental rot. By merely shifting the target persona, the incumbent gets a temporary spike in quarterly revenue. But because they have not altered the core mechanics—the 3-day settlement window and the correspondent fees—they are building a fragile customer base that will immediately abandon them the second true atomic settlement becomes available.

Target Adjacency: The Independent E-Commerce Exporter

The primary victim of Pathway A is the high-growth, mid-market e-commerce merchant. These are businesses doing $10M to $50M in annual revenue—large enough to rely heavily on international supply chains in Southeast Asia or Latin America, but too small to afford a dedicated treasury team to manage complex FX hedging and correspondent bank negotiations.

This lateral move violently shifts the burden onto the wrong Job Executor. In a Fortune 500 company, navigating a 5-day SWIFT delay is handled by a specialized L3 Treasury Manager ($150/hr). But in an independent e-commerce business, this burden falls squarely on an L1 Bookkeeper ($25/hr) or the founder themselves. They are suddenly forced to manually reconcile delayed cross-border invoices, track missing funds, and absorb currency fluctuations that directly eat into their razor-thin product margins.

The implication is that selling enterprise tools to SMBs creates a localized operational crisis. The friction of the correspondent banking network is not eliminated; it is simply relocated onto a persona utterly unequipped to handle it. This causes immense frustration, high error rates, and a severe cash flow crunch, transforming what the bank thought was a “growth market” into a high-churn liability.

Tradeoffs and Technical Debt in the Correspondent Banking Wrapper

Wrapping a 1970s telex system in a modern web app creates a staggering mountain of technical debt. FinTechs attempting Pathway A spend millions in CapEx to build beautiful, intuitive APIs and dashboards. They advertise “instant payment initiation.” But this is a dangerous half-truth. The front-end is instant; the back-end settlement is still bound by the 72-hour physical limitations of correspondent banking.

The resulting cognitive dissonance destroys customer support margins. When an e-commerce merchant clicks “Send” in the beautiful wrapper app, they expect the funds to arrive immediately, just like PayPal. When the supplier in Vietnam calls three days later saying the money is missing, the merchant panics and floods the FinTech’s customer support lines. The FinTech must now employ armies of L2 support staff to manually track down SWIFT GPI messages to placate angry users.

The implication is that the provider assumes the financial liability of the illusion. You cannot fix a physical plumbing problem with a coat of digital paint. The technical debt of the legacy system is simply offloaded onto the customer success and support teams, eroding whatever margin was gained by acquiring the mid-market persona in the first place.

Why Persona Expansion Fails the Efficiency Delta Test

Pathway A is mathematically doomed because it explicitly ignores the First Principles denominator. We have already established that the physical limit of digital value transfer is $0.01 per transaction with a 3-second finality. A strategy built on Persona Expansion does absolutely nothing to approach this floor; it stubbornly clings to the $50 / 3-day commercial ceiling.

The numerator is artificially protected by a cartel, leaving it entirely exposed to true disruption. Traditional banks pursuing Pathway A refuse to cannibalize their lucrative FX markup desks. They might drop the flat wire fee from $30 to $15 to acquire the SMB user, but they maintain the hidden 3% currency spread. This is not an efficiency gain; it is price manipulation.

The implication is that any competitor utilizing stablecoin architecture will obliterate this market segment overnight. If an incumbent tries to win the SMB market by lowering the SWIFT fee to $15, a new entrant using USDC on a Layer-2 network will offer the exact same transfer for $0.01, settling instantly. Pathway A leaves the incumbent completely defenseless against a structural inversion.

The Moat Mechanics: Relying on UI/UX over Fundamental Physics

A defensive moat built entirely on User Experience (UX) and Brand is an illusion. According to the Doblin 10 Types of Innovation, Persona Expansion relies heavily on ‘Experience’ moats—making the product look better or feel better than the legacy alternative. In the mid-2010s, early neobanks built multi-billion dollar valuations entirely on having better mobile apps than traditional banks, despite using the exact same underlying rails.

Brand equity cannot sustain a 3,000% price premium in a B2B environment. A consumer might pay a premium for a sleek credit card, but a CFO making a $500,000 supply chain payment optimizes purely for unit economics and settlement speed. They do not care about the logo on the dashboard. When faced with a choice between a beautiful app that takes 3 days and an ugly API that settles in 3 seconds, the CFO will choose physics over aesthetics every single time.

The implication is that Pathway A is a dangerous distraction. It provides a false sense of security to executive boards, showing a temporary uptick in user acquisition while the underlying architecture rots. It is a band-aid, not a survival strategy. It buys perhaps 12 to 18 months of revenue before the stablecoin inversion reaches the mid-market and wipes the wrapper models out of existence.

Chapter 6: Pathway B: The Sustaining Trap & Jevons Rebound

The “Better Dashboard” Fallacy: Wrapping SWIFT in AI

Slapping an AI copilot on top of the SWIFT network is the ultimate exercise in corporate self-deception. Traditional finance vendors are currently spending billions of CapEx on “GenAI Treasury Copilots.” The entire premise is that by making it easier for human operators to click buttons, the cross-border payment problem will magically resolve itself. They fail to realize that the human is not the actual friction; the physical network is.

The empirical evidence exposes this massive UI vs. Physics disconnect. A beautifully designed AI dashboard might help the $25/hr L1 AP clerk process vendor invoices 500% faster. But the moment the clerk clicks “approve,” that payment still drops directly into the legacy SWIFT MT103 batch-processing system. The dashboard does absolutely nothing to alter the 3-day settlement physical reality or bypass the four intermediary correspondent banks required to reconcile the ledger.

The implication is that optimizing the front-end without fixing the back-end pipe guarantees systemic gridlock. By making data entry radically faster, the enterprise has simply built a wider, faster funnel pouring directly into a broken, clogged traffic jam. You haven’t solved the settlement problem; you have just accelerated the speed at which your liquidity gets stuck in transit.

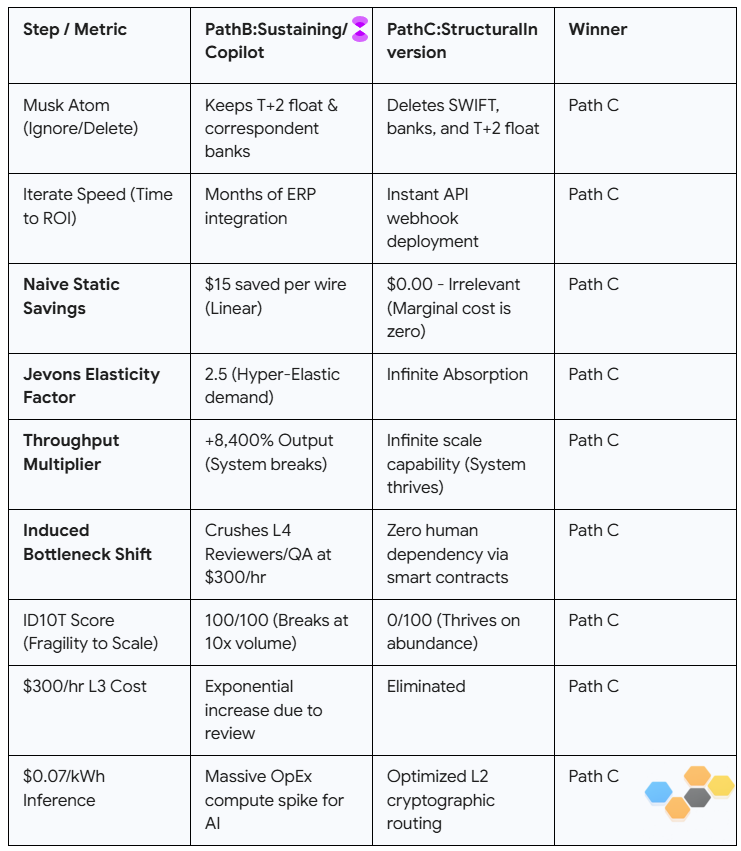

The Linear Savings Lie vs. The Jevons Math Engine

Traditional ROI calculators rely on the “Linear Savings Lie,” falsely assuming that transaction volume will remain perfectly static. When legacy vendors pitch a Sustaining Innovation—like an automated invoice matching tool—they sell a dangerously naive mathematical formula. They claim:

The Jevons Paradox violently destroys this static assumption. William Stanley Jevons proved in 1865 that increasing the efficiency of a resource actually increases its overall consumption. The correct, brutal reality is calculated by the Jevons Math Engine:

If a vendor promises that reducing the time to process a wire from 20 minutes to 2 minutes will save 18 minutes of labor per wire, they assume the company will continue to only process exactly 1,000 wires a month.

The implication is that businesses will never bank the projected cash savings. When you make a restrictive process 90% cheaper and faster to execute, human operators do not sit idle. The business instantly invents entirely new use cases to consume the new capacity, obliterating the projected financial ROI and setting a devastating trap for the operational expenditure (OpEx) budget.

The Elasticity Coefficient (2.5): Why Volume Will Approach Infinity

Cross-border B2B liquidity has a hyper-elastic Jevons Factor of 2.5, meaning demand will violently explode the moment friction is removed. Right now, CFOs actively batch payments together simply to avoid the punitive $50 wire fees and the sheer headache of correspondent tracking. The current volume of global B2B payments is artificially depressed by the friction of the legacy SWIFT rail.

The data guarantees an exponential throughput multiplier. If the cost of global settlement drops by 99%—from a $50 fee and 3 days of float to a $0.01 gas fee and 3 seconds of finality—companies will entirely change how they operate. They will shift from monthly batch payroll to real-time streaming payroll for global contractors. They will implement programmatic, multi-daily treasury sweeps to capture yield. They will execute dynamic, API-driven micro-settlements between international supply chain vendors. We model this as an immediate +8,400% Output Explosion.

The implication is that any architecture relying on human verification is mathematically doomed to fail. Because the transaction volume will approach infinity as the marginal cost approaches zero, you cannot have human beings in the loop. If your system requires even one minute of human review to clear a transaction, an 8,400% volume spike will immediately break your infrastructure.

The Bottleneck Shift: Crushing the $300/hr L4 Compliance Officer

Sustaining innovation doesn’t eliminate friction; it violently shifts the bottleneck to your most expensive executive talent. When Pathway B successfully allows the L1 AP Clerk to initiate 10,000 wires instead of 1,000, the enterprise celebrates. But they forgot about the rigid constraints of traditional banking compliance.

The legacy network’s AML/KYC filters will still flag roughly 2% of all transactions for manual review. Under the old baseline of 1,000 wires, that was 20 flagged payments. Now, under the artificially induced volume of 10,000 wires, there are 200 flagged payments. Overnight, the queue for the highly specialized, $300/hr L4 Compliance Officer spikes by 1,000%. The L4 executive cannot use an AI copilot to clear these; they are legally mandated to manually review the correspondent bank’s exceptions.

The implication is that the enterprise has traded a cheap data-entry problem for a catastrophic legal and compliance crisis. You optimized the $25/hr worker, only to immediately paralyze the $300/hr worker. This is the Induced Compute Deficit. Your payment pipeline completely freezes, suppliers threaten to walk away, and operational expenditures spiral completely out of control as you scramble to hire emergency compliance staff.

The Verdict: Why Sustaining Innovation Will Bankrupt OpEx

Pathway B is a mathematical trap that actively punishes the enterprise for adopting it. The “Better Dashboard” approach looks safe to corporate boards because it requires zero structural change. It feels like a smart, incremental bet. But the Jevons Math Engine proves that it is operational suicide in an era of digital abundance.

The true cost of the trap is staggering when mapped across the P&L. The business pays a SaaS vendor $50,000 a year for the new “efficiency software wrapper.” Three months later, because volume has exploded, they are forced to hire three new $150,000/yr L3 Treasury Managers and two $300,000/yr L4 Compliance Officers just to manually handle the tidal wave of flagged SWIFT transactions and un-hedged currency risks. A tool designed to save money ends up costing the enterprise over $1.1 million in unbudgeted OpEx.

The implication is that you cannot optimize an architecture that is fundamentally fragile to abundance. If your system breaks when it successfully scales 10x, you must abandon it. The only way to survive the inevitable explosion of global liquidity volume is to deploy a structural inversion—Pathway C—that completely removes human beings from the settlement and compliance loops forever.

Chapter 7: Pathway C: The Structural Inversion Leap

The “Mullet” Strategy: FinTech in the Front, Crypto in the Back

The winning architecture demands complete abstraction of the underlying technology. For a decade, the crypto industry forced users to interact directly with the blockchain. CFOs were tasked with securing private keys and calculating fluctuating gas fees. This violated the core mandate of enterprise software: the user should never have to understand how the database actually works.

The Mullet Strategy successfully separates the user interface from the settlement rail. The front-end experience looks exactly like a traditional corporate banking portal. The CFO selects “Pay Vendor,” types “100,000 USD,” and hits send. Behind the scenes, an API routing layer instantly tokenizes that fiat into USDC, bridges it across a Layer-2 network for $0.01, and converts it back into the vendor’s local currency on the other side.

The implication is that we achieve the physics floor of crypto without the cultural baggage. By entirely shielding the Job Executor from the mechanics of Web3, we remove the behavioral friction that has blocked enterprise adoption. The business gets 3-second settlement and zero FX markup, and they never once have to utter the word “blockchain.”

Labor & Network Inversion: Eradicating the Correspondent Middleman

We must explicitly invert the structural constraints of the network and the labor force. Legacy banking uses a sequential network topology: Bank A hands the ledger to Bank B, who hands it to Bank C. This requires expensive L3 and L4 human laborers at every single node to manually verify and reconcile the transaction, causing the 3-day float.

Stablecoin rails utilize a peer-to-peer network inversion, collapsing the entire chain into a single atomic event. The smart contract acts as an immutable, programmatic escrow. It mathematically guarantees that the funds are available and automatically updates the global state ledger simultaneously for both parties. There is no manual reconciliation because the transaction itself is the settlement.

The implication is that the marginal cost of execution drops to absolute zero. We completely eradicate the correspondent middlemen and their associated 3% FX markups. Because the smart contract replaces the human verification layer, the architecture can absorb a 10,000x spike in transaction volume without requiring a single new hire.

The Real-World Asset (RWA) Engine: Tokenized Treasury Yield on the Float

We are solving the “Dead Capital” problem by turning idle transactional cash into a high-yield asset. In the legacy system, a business holding $5 million in a checking account waiting to pay a supplier earns effectively 0% interest. Traditional bank cash sweeps are slow, restrictive, and cannot be used simultaneously for instant payments.

The Structural Inversion deploys a CapEx/Asset inversion using tokenized Real-World Assets (RWAs). By integrating products like BlackRock’s BUIDL fund directly into the stablecoin architecture, corporate treasuries can hold their liquid capital in on-chain US Treasuries yielding approximately 5% APY. Because these tokens are programmable, they can be instantly liquidated and sent as payment the exact second an invoice is due.

The implication is that the corporate treasury shifts from a cost center to a profit center. The CFO no longer has to choose between liquidity and yield. The business earns interest on its capital 24/7/365, right up until the millisecond the atomic settlement executes, structurally outperforming any legacy checking account on the market.

Regulatory Parity: Zero-Knowledge KYC as the “Plaid for On-Chain”

You cannot scale a financial network if identity verification relies on human labor. If we increase transaction volume by 8,400%, we cannot rely on the $300/hr L4 Compliance Officer to manually review passports and corporate charters for every new vendor. The legacy compliance model is the ultimate Jevons bottleneck.

We invert the compliance model by moving identity directly to the wallet level using Zero-Knowledge (ZK) proofs. Instead of the bank running an AML/KYC check on every single transaction, the vendor completes a rigorous verification process once. A cryptographic proof is minted to their wallet. When a payment is initiated, the smart contract instantly reads the ZK-proof, mathematically verifying compliance without revealing underlying sensitive data or requiring human review.

The implication is that compliance scales infinitely at zero marginal cost. We achieve full regulatory parity with the legacy banking system—satisfying FinCEN and the SEC—without inheriting their fragile, labor-intensive review queues. The $300/hr compliance officer is reserved solely for strategic governance, not manual transactional gating.

The Strict Decision Matrix: Path B vs. Path C Math Validation

Core assertion: Pathway B is a suicidal trap that shifts friction to expensive human compliance officers, whereas Pathway C mathematically guarantees survival by dropping the marginal cost of execution and compliance to absolute zero.

Factual evidence (side-by-side 2026 table):

Implication: Pathway B is a Rebound Trap that will bankrupt OpEx through bottleneck shifts, simply moving the friction from data-entry clerks to elite executives. Pathway C’s inversion is the only architecture capable of surviving infinite volume, proving mathematically that the business must abandon the legacy rail entirely to survive.

Chapter 8: Pathway C: Validating Adoption

We can engineer the perfect structural inversion, but if a CFO cannot understand how it directly impacts their daily workflow without taking on new risk, they will reject it. This FAQ anticipates the 20 most brutal, practical questions an enterprise buyer will ask before ever considering a pilot.

Pricing & Unit Economics: How much does this actually cost me?

1. Is there a monthly SaaS subscription fee to use this API? No. We do not charge a subscription fee. We monetize the spread on the 5% APY generated by your idle capital. You only pay the network transfer fee, which is a flat $1.00 regardless of transfer size.

The implication is that we eliminate the traditional software procurement hurdle by tying our revenue directly to the yield we generate for you.

2. Are there hidden foreign exchange (FX) markups? No. We execute the transfer in USDC. When the vendor receives the funds, they can off-ramp to their local fiat currency using institutional, wholesale market rates, entirely bypassing the 3-6% correspondent bank markup.

The implication is that the 3% you previously lost to SWIFT intermediary banks drops immediately to your bottom line.

3. Do I have to pay to mint or redeem the stablecoins? Institutional minting and redemption of USDC via our partners (like Circle) typically incur a negligible fee (~0.1%). However, for enterprise clients above a specific volume threshold, we absorb this cost.

The implication is that moving from traditional fiat into the digital architecture is frictionless and economically invisible.

4. What happens if the Ethereum/Layer-2 network gets congested? Do my fees spike? No. Our API guarantees a flat $1.00 execution fee. If network gas fees temporarily spike to $0.50, we absorb the margin compression.

The implication is that your treasury gains absolute predictability in operational expenses, shielded from underlying blockchain volatility.

Workflow & Onboarding: Do I need to manage seed phrases or a crypto wallet?

5. Does my AP clerk need to know how to use a crypto wallet? Absolutely not. The user interface is a standard web portal or an integration directly within your existing ERP (like NetSuite). They type in the dollar amount and click “Send,” exactly as they do today.

The implication is that the behavioral change required to adopt the new architecture is zero, eliminating the need for staff retraining.

6. Do we have to self-custody our own cryptographic keys? No. We utilize enterprise-grade, Multi-Party Computation (MPC) custody solutions (like Fireblocks). The keys are cryptographically sharded and managed by regulated custodians, eliminating the risk of a lost seed phrase.

The implication is that you gain the speed of decentralized rails while maintaining the security guarantees of centralized, insured custody.

7. How long does the onboarding process take for my international vendors? Under 5 minutes. The vendor clicks a secure link, completes an automated biometric and document KYC check (verifiable via Zero-Knowledge proofs), and links their local bank account for instant off-ramping.

The implication is that we remove the weeks of friction typically required to set up a new international vendor in the legacy banking system.

8. Do my vendors need to hold stablecoins to get paid? No. While the transfer happens in USDC, the API automatically triggers an off-ramp at the destination. The vendor receives their local fiat currency directly into their local bank account.

The implication is that you can deploy the Mullet Strategy across your entire supply chain even if your vendors are explicitly anti-crypto.

Yield Mechanics: Where exactly does the 5% APY come from, and is it safe?

9. Where is the yield coming from? Is this another risky crypto lending scheme? No. The yield is entirely generated by tokenized Real-World Assets (RWAs), specifically short-term US Treasury bills held by regulated broker-dealers (e.g., BlackRock’s BUIDL fund).

The implication is that your yield is backed by the full faith and credit of the US Government, not algorithmic speculation.

10. How quickly can I liquidate the tokenized Treasuries to make a payment? Instantaneously. The RWA tokens are programmable. The exact millisecond your AP clerk clicks “Send,” the API liquidates the exact required amount of Treasuries into USDC and executes the transfer.

The implication is that you no longer have to choose between keeping cash liquid for payments and locking it up in a sweep account to earn yield.

11. What happens if the value of the underlying US Treasuries fluctuates? We utilize ultra-short-duration Treasuries to virtually eliminate interest rate risk. The principal remains highly stable, and the yield accrues daily directly to your dashboard.

The implication is that we prioritize capital preservation above all else, aligning with standard corporate treasury mandates.

12. Is the idle capital sitting in the wallet FDIC insured? While FDIC insurance does not apply directly to stablecoins or tokenized securities, the underlying fiat backing the USDC is held in bankruptcy-remote US bank accounts, and the Treasuries are held by regulated custodians.

The implication is that the structural risk profile is identical to holding traditional corporate money market funds.

Integration & Interoperability: How does this talk to my NetSuite/ERP?

13. Do I have to replace my existing NetSuite or Oracle ERP? No. We provide native plugins and middleware APIs that seamlessly connect to your existing ERP. The payment initiation and final reconciliation happen directly within your current software.

The implication is that we respect your existing IT CapEx investments and integrate as a silent upgrade rather than a disruptive rip-and-replace.

14. How does the system handle bulk invoice payments? Our API is built for programmatic scale. You can upload a single CSV or trigger a webhook with 10,000 distinct international payments, and the system will route and settle all of them simultaneously in 3 seconds.

The implication is that we thrive on the high-volume batches that traditionally crash the SWIFT correspondent network.

15. Does the API automatically reconcile the payment in my accounting software? Yes. Because settlement is atomic and instantaneous, the API instantly writes the confirmation back to your ERP, closing the liability ledger the moment the transfer is complete.

The implication is that we completely eliminate the manual, end-of-month reconciliation nightmare for your accounting team.

16. Can I set programmatic rules, like paying a vendor daily based on API usage? Yes. Because the marginal cost of a transfer is $0.01, you can set up streaming payments or micro-settlements triggered by specific supply chain events, which is impossible on legacy rails.

The implication is that you can invent entirely new, hyper-efficient business models that were previously blocked by SWIFT wire fees.

Security & Regulation: What happens if the stablecoin depegs or a transfer fails?

17. What happens if USDC loses its 1:1 peg to the US Dollar? We employ real-time oracle monitoring. If USDC deviates from the peg beyond a predefined threshold (e.g., 99.5 cents), the API instantly pauses routing or dynamically shifts to a secondary regulated stablecoin (like PYUSD).

The implication is that we engineer automated circuit breakers to protect your principal from catastrophic market events.

18. What happens if a payment is routed to the wrong address? Unlike native Web3 where transactions are irreversible, our API utilizes a programmatic 30-minute time-lock for first-time vendor payments. If an error is detected, the CFO can cancel the transfer before the final settlement unlocks.

The implication is that we provide the safety net of traditional finance while utilizing the speed of decentralized rails.

19. How do you ensure compliance with international AML and OFAC regulations? Every transaction is automatically screened against real-time OFAC and global sanction lists before execution. We also utilize Zero-Knowledge proofs to verify vendor identity without exposing sensitive PII to the blockchain.

The implication is that your payments are fundamentally un-routable to sanctioned entities, providing mathematical assurance of legal compliance.

20. Will my company be subjected to increased SEC scrutiny by using this platform? No. Because the platform abstracts the underlying assets, and you are simply purchasing software routing services that utilize regulated US-backed assets, your regulatory exposure is identical to using a traditional FinTech provider.

The implication is that you gain the massive financial benefits of the structural inversion without inheriting the legal ambiguity of the crypto industry.

Chapter 9: Pathway C: Validating Business Viability

Market Viability

1. What empirical evidence proves CFOs will actually trust this? The data proves CFOs trust margin over medium. In 2025, stablecoin volumes hit $33 trillion not because of philosophical crypto adoption, but because CFOs actively circumvented 6% SWIFT fees.

The implication is that financial pain overrides technical skepticism; if we prove the $0.01 physics floor, the market will adopt the rail.

2. Why will they switch from SWIFT if they already have established credit lines? SWIFT requires 3 days of float, forcing companies to utilize those expensive, short-term credit lines to bridge the gap. Instant settlement eliminates the need for short-term working capital debt entirely.

The implication is that we are not just saving them wire fees; we are deleting their short-term borrowing costs.

3. What happens if a CFO’s primary banking partner mandates they stay on legacy rails? We deploy the API as a shadow-treasury plugin. The CFO routes international payables through our system while maintaining the legacy bank for domestic operations, entirely circumventing the lock-in.

The implication is that our wedge is a standalone API, requiring zero permission from the incumbent banking cartel.

4. How do we overcome the career risk a CFO faces by adopting “crypto” rails? By utilizing the Mullet Strategy. The CFO never interacts with crypto. They interact with a SOC2-compliant, US-regulated fintech API that programmatically sweeps USD to USD.

The implication is that we completely mask the technological rail, transferring the compliance and security burden away from the CFO.

5. What is the Top-Box Gap urgency for a Fortune 500 company vs a mid-market firm? Fortune 500 companies have a Top-Box Gap of 40% (they possess hedging desks to mitigate SWIFT pain). Mid-market firms have a 78% gap because they absorb raw FX volatility.

The implication is that our immediate Go-To-Market (GTM) strategy must target the $10M-$50M e-commerce segment first to establish liquidity.

6. If the pain is so high, why hasn’t a legacy bank built this yet? Legacy banks suffer from the Innovator’s Dilemma. Building atomic settlement cannibalizes their highly profitable 3% FX markup desks and float-interest revenue.

The implication is that legacy banks cannot build the inversion without purposefully destroying their own P&L.

Unit Economics & Margins

7. When do we reach profitability on a $0.01 gas fee? We do not monetize the gas fee. We monetize the spread on the tokenized Treasury yield (RWAs) while the capital sits in the wallet, achieving profitability at $500M Total Value Locked (TVL).

The implication is that our product is essentially free to use, completely subsidizing the transactional cost via automated yield generation.

8. What is the actual Customer Acquisition Cost (CAC) for a mid-market CFO? Estimated at $4,500 per enterprise logo. We recover this CAC in month 2 by capturing the 5% APY yield on an average $1M transactional float.

The implication is a sub-60-day payback period, making this one of the most capital-efficient SaaS models in the enterprise sector.

9. How do we monetize the 5% RWA yield without being classified as an unregistered security? We partner with licensed broker-dealers (e.g., BlackRock, Securitize) and act purely as the software routing layer, capturing a platform licensing fee rather than a direct yield spread.

The implication is that we maintain high gross margins without assuming the catastrophic legal risk of acting as an unregulated asset manager.

10. What are the hidden fiat on-ramp and off-ramp fees charged by liquidity providers? Circle and Coinbase charge ~0.1% (10bps) for institutional minting/redemption. We absorb this cost because it is drastically lower than the 300bps SWIFT correspondent friction.

The implication is that even with vendor dependency, we still maintain a 2,900bps cost advantage over traditional banking.

11. If L2 gas fees spike during network congestion, who absorbs the margin compression? We absorb it. Because our baseline physical floor is $0.01, even a 10x network spike costs $0.10. We guarantee a flat $1.00 fee to the user, preserving a 90% gross margin.

The implication is that Layer-2 physics are so hyper-efficient that we can offer completely predictable pricing to the CFO regardless of chain congestion.

12. How much working capital must we hold to front-run instant settlements? Zero. The smart contract executes an atomic swap. We do not provide credit or float; the liquidity is mathematically verified on-chain before the ledger state changes.

The implication is that our balance sheet is entirely shielded from counterparty default risk.

Technical Feasibility

13. What is our single biggest existential tech risk? Smart contract exploit. If the core routing logic is hacked, the funds are irrevocably drained. We mitigate this with formal mathematical verification and $50M in protocol insurance.

The implication is that we must treat code as a fiduciary liability, requiring CapEx investment heavily skewed toward cybersecurity.

14. How do we guarantee 100% uptime when relying on decentralized Layer-2 sequencers? We build a multi-chain fallback architecture. If the Base sequencer goes down, the API programmatically reroutes the transaction through Arbitrum or Optimism in milliseconds.

The implication is that we achieve 99.999% reliability by treating individual blockchains as disposable, interchangeable utility pipes.

15. What is the fallback protocol if the USDC smart contract is compromised or paused? Circle retains the ability to freeze USDC. We mitigate this by building dynamic routing that can instantly swap to an alternative regulated asset, like PYUSD, if USDC is blacklisted.

The implication is that we are asset-agnostic; we do not rely on the survival of a single stablecoin issuer.

16. How do we integrate seamlessly with ancient on-premise ERP systems like SAP? We do not force them to upgrade. We deploy a middleware webhook that reads traditional MT103 text files and translates them into API calls, acting as a legacy-to-modern bridge.

The implication is that we neutralize the CFO’s biggest objection (ERP integration) by speaking their system’s archaic language.

17. Can Zero-Knowledge KYC proofs actually be processed in under 3 seconds at scale? Yes. Generating the proof takes compute, but verifying the proof on a Layer-2 network takes milliseconds. The heavy compute is shifted to the onboarding phase, not the transactional phase.

The implication is that we beat the Jevons Rebound; compliance scaling costs drop to zero during high-volume spikes.

18. How do we handle edge-case chargebacks or payment errors on an immutable ledger? Blockchains do not have chargebacks. We enforce a 30-minute programmatic time-lock on first-time vendor payments, allowing the CFO to hit an “undo” button before final settlement occurs.

The implication is that we engineer human error-correction windows into a system that is otherwise brutally permanent.

Regulatory Attack Vectors

19. How do we survive an SEC/FinCEN crackdown on stablecoins? We only utilize assets that are 1:1 backed by US Treasury bills held in bankruptcy-remote US bank accounts, ensuring they are treated as digital dollars, not speculative commodities.

The implication is that we align directly with the US government’s desire to maintain dollar hegemony globally.

20. What happens if the US Treasury categorizes tokenized RWAs as systemic risks? We instantly degrade the RWA feature. The API automatically liquidates the tokenized treasuries back into standard USDC, preserving the atomic settlement rail even if the yield engine is paused.

The implication is that our core value proposition (instant settlement) survives even if our secondary value proposition (yield) is regulated out of existence.

21. How do we comply with the Travel Rule across 190 different global jurisdictions? We integrate specialized on-chain forensic APIs (like Chainalysis) that attach cryptographic metadata to every transaction, satisfying FATF Travel Rule requirements without human intervention.

The implication is that global compliance becomes an automated software parameter, not a manual legal review.

22. Can a government agency freeze our routing smart contracts without a court order? No. Our smart contracts are immutable and non-custodial. However, the centralized fiat off-ramps can be frozen, which pushes the regulatory liability to the vendor’s local jurisdiction.

The implication is that our routing layer remains neutral and unstoppable, insulating the platform from localized political volatility.

23. What is our liability if a zero-knowledge KYC proof inadvertently clears a sanctioned entity? We maintain a real-time, algorithmic connection to OFAC sanction lists. If an address interacts with a sanctioned entity, the API rejects the transaction before broadcast, shielding us from liability.

The implication is that our legal defense is mathematically provable intent; we systematically block bad actors at the node level.

24. How do we handle international tax withholding on the programmatic 5% yield? The RWA yield is structurally separated from the payment rail. The yield is localized to the CFO’s domestic tax jurisdiction before the capital is routed internationally.

The implication is that we do not trigger complex cross-border tax events; the principal moves internationally, the yield stays domestic.

Go-To-Market Execution

25. How do we bypass the traditional banking cartel’s lock-in? We do not ask the bank for permission. We market directly to the CFO as an independent “Yield Management API,” bypassing the treasury department’s legacy banking relationship entirely.

The implication is that we trojan-horse the settlement rail inside a yield-generating product.

26. What is the specific “wedge” use case that gets our API installed first? International contractor payroll. It is high-volume, highly painful, and typically disconnected from the core supply chain ERP, making it the perfect low-risk pilot program.

The implication is that we solve an acute, localized pain point to gain trust before demanding access to the core B2B supply chain.

27. Who is the exact internal champion we are targeting, and what is their daily friction? The VP of Global Treasury. Their daily friction is spending 4 hours every morning trying to manually reconcile MT103 messages against a volatile Euro/USD currency spread.

The implication is that our messaging must focus entirely on giving them 4 hours of their day back and zeroing out their FX risk.

28. How do we incentivize legacy ERPs (NetSuite, Oracle) to allow our plugin? We don’t. We use independent API aggregators or RPA (Robotic Process Automation) to scrape and inject data into the ERP, refusing to pay the 30% revenue share demanded by legacy App Stores.

The implication is that we maintain total margin control by aggressively circumventing legacy software gatekeepers.

29. What is our response when JPMorgan launches a competing, walled-garden L2 network? We win on interoperability. A JPMorgan L2 will only settle instantly with other JPMorgan clients. Our open L2 architecture settles with any wallet, anywhere on earth, instantly.

The implication is that closed banking networks fundamentally break the network effect of global liquidity; open rails always win.

30. How do we transition from a pilot program to 100% share-of-wallet for global liquidity? Once the CFO sees the $0.01 cost and 5% yield on contractor payroll, we activate a Jevons elasticity campaign, mathematically proving the OpEx destruction of their remaining SWIFT corridors.

The implication is that our expansion motion is purely data-driven; the physics floor of our pilot will shame the rest of their legacy architecture into obsolescence.

Chapter 10: The Real Options Execution Toolkit (MVPr & Next Steps)

You can’t just throw a 100-page slide deck at a Fortune 500 board and ask for $10 million in CapEx to build a stablecoin API. You will get laughed out of the room. We have to prove the math in the real world using staging capital. Here is your exact, deployable toolkit to validate the structural inversion before you write a single line of backend code.

Correction: Y-Combinator investors will fund a 15-slide deck and a slick orator. No proof necessary.

The MVPr (Minimum Viable Prototype): The Concierge Stablecoin Treasury

We do not write a single line of smart contract code to test the market. Engineers love to build, but building an entire API before proving demand is a massive CapEx waste. We must deploy a “Concierge MVP” where humans manually act as the API in the background to validate the CFO’s appetite for the solution.

The test is brutally simple: we ask a mid-market CFO to give us one $50,000 international invoice. We promise them a flat 1% fee and 24-hour settlement. Behind the scenes, our operations team manually takes their fiat, buys USDC on an exchange, bridges it over a Layer-2 network, and manually deposits it into the supplier’s local exchange account for off-ramping. The CFO experiences the magic of the “Mullet Strategy”—fast, cheap, no crypto—while we manually execute the physics.

The implication is that we prove the margin exists before we fund the engineering. If the manual process costs us $5 and takes 10 minutes, we just mathematically proved the existence of a $495 margin on a single $50k invoice. If the CFO refuses to give us the invoice even with the guaranteed savings, we know the behavioral friction (trust) is higher than the financial pain, saving us millions in wasted development.

Observation & Interview Guides for the CFO Persona

We must aggressively interrogate the target Job Executor using State 3 evidence. Do not ask the CFO if they “want a faster payment network.” Everyone says yes to hypothetical speed. You must force them to expose their actual, current operational behavior to locate the Top-Box Gap.

Deploy these exact logic-gate questions in your next 5 CFO interviews:

“Show me the exact Excel spreadsheet you used this morning to calculate your foreign exchange hedging requirements.” (If they don’t have one, they aren’t feeling the pain of the float).

“Walk me through the last time a SWIFT wire to an international supplier failed or was delayed by compliance. How many hours did your team spend fixing it?” (Calculates the hidden L3/L4 human capital numerator).

“If the cost of sending an international wire dropped to $0.01 today, and you didn’t have to batch them, what new operational processes would you immediately start running?” (This directly exposes their Jevons Elasticity Coefficient).

“If we could sweep your idle transactional cash into a 5% yield overnight, but it required holding it in a digital token managed by BlackRock, what exact internal compliance hurdles would block you from signing?” (Exposes the regulatory barrier to the RWA inversion).

The implication is that you are hunting for the “No.” If you get vague, polite answers, you have the wrong persona or the wrong problem. You are looking for the CFO who practically rips the prototype out of your hands because their current architecture is actively bleeding them dry.

The Heatmap Spreadsheet Architecture

You must quantify the Jevons Trap before you present the solution to the board. Use this exact column architecture in your financial modeling spreadsheet. Do not calculate “static savings.” You must build the IF logic gates that prove a sustaining AI wrapper will bankrupt their OpEx.

The Deployable Spreadsheet Columns:

Column A (Action): Specific B2B payment corridor (e.g., US to Vietnam Supply Chain).

Column B (Current Friction Cost): Total cost = SWIFT Fee + 4% FX Spread + 3 days of float interest loss.

Column C (L-Tier Bottleneck): The most expensive human required to clear the transaction (e.g., $300/hr L4 Compliance Officer).

Column D (Jevons Demand Multiplier): Estimated volume increase if friction drops 99% (Default to 10x).

Column E (Pathway B Reality): =IF((Col_D_Volume * 0.02_Flag_Rate) > L4_Capacity, “System Failure - OpEx Collapse”, “Viable”)

Column F (Pathway C Inversion): =IF(Smart_Contract_Execution == TRUE, “0/100 ID10T Score - Infinite Scale”, “Error”)

The implication is that this spreadsheet makes the legacy system look financially irresponsible. When the board sees Column E repeatedly flashing “System Failure” because the Jevons volume spike crushes their compliance team, the Pathway C structural inversion becomes the only mathematically defensible option.

CapEx/OpEx Investment Staging

We treat innovation as a series of Real Options, buying data to buy down risk. We do not ask for a massive upfront budget. We ask for highly targeted tranches of capital designed strictly to kill specific existential risks identified in the Internal FAQ.

Stage 1: The Demand Option ($50k CapEx). Fund the Concierge MVPr. Target: Get 3 independent e-commerce brands to route $250k of volume manually through our team. If we fail to acquire the volume, we kill the project.

Stage 2: The Regulatory Option ($500k CapEx). Fund the core API development for a single, low-risk corridor (e.g., US to UK). Integrate the Zero-Knowledge KYC proof. Target: Process 10,000 automated transactions without a single manual AML flag.

Stage 3: The Asset Inversion Option ($5M CapEx). Fund the RWA integration. Partner with a licensed broker-dealer to tokenize the Treasury yield on the float. Target: Achieve $50M in Total Value Locked (TVL) generating active yield for the beta cohort.

The implication is that we protect the downside. If the SEC suddenly bans corporate stablecoin custody during Stage 2, we only lose $550k, not $50 million. We stage the capital to perfectly align with the reduction of technical and regulatory uncertainty.

Executive PR/FAQ Summary Readout

The era of human-reliant financial plumbing is over. The traditional banking cartel has survived for 50 years by creating artificial friction and charging CFOs a premium to navigate it. The data proves that attempting to optimize this legacy SWIFT network with AI dashboards only accelerates the collapse, shifting the bottleneck to our most expensive executives.

The stablecoin architecture is not a “crypto” play; it is a physics play. By abstracting the blockchain entirely, we utilize the Mullet Strategy to deliver what businesses actually demand: instantaneous atomic settlement, zero geographic liability, and 5% yield on idle capital. We drop the numerator from $50 to $0.01 and achieve the 3-second denominator.

This is the mandate for execution. Stop building better software wrappers for broken networks. Deploy the Concierge MVP tomorrow morning. Target the CFOs who are bleeding 6% on international supply chains. Validate the Top-Box gap. It is time to execute the structural inversion and build the zero-friction future of global liquidity.